Tuesday February 11, 2025

Covid and Consumer Behavior

How COVID-19 Changed Retail Buying Patterns

What happens in retail is largely a byproduct of the overall economy, consumer behavior, and consumer discretionary income—that is, how much “free money” a person has. Regardless of a consumer’s desire to buy, if they lack the financial resources (due to unemployment, reduced credit, etc.), spending will naturally decline. Conversely, consumers with robust bank accounts have a greater capacity to spend.

COVID-19 was a formative event in our collective history—comparable in impact to moments like the JFK assassination or the moon landing. The experience of the pandemic is indelibly etched in our memories, and its effects on consumer behavior are still being unraveled.

Observing the Change

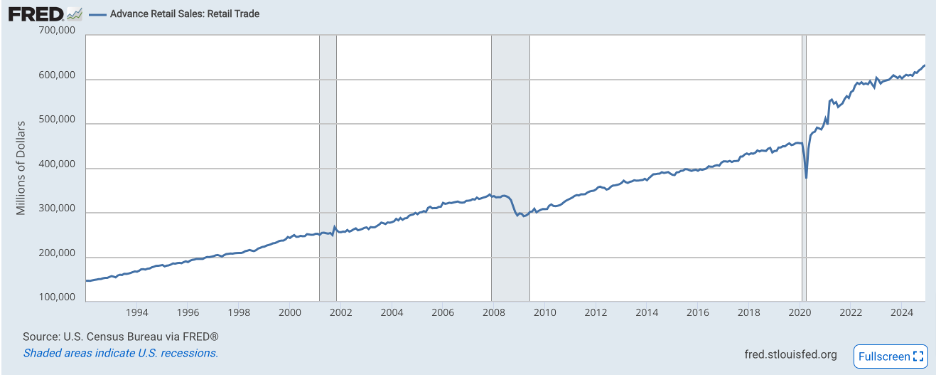

Each month, the government releases data on “Retail Sales,” which measures the total money spent in retail across the U.S. While retail sales have generally trended upward over the years, there was a significant dip during the COVID-19 lockdowns. When economies shut down and people were required to stay home for several months, consumer behavior had to adapt rapidly.

With physical stores closed or operating under strict social distancing guidelines, consumers were left with two main options:

- Shop in-person for the categories that remained open.

- Switch to online shopping.

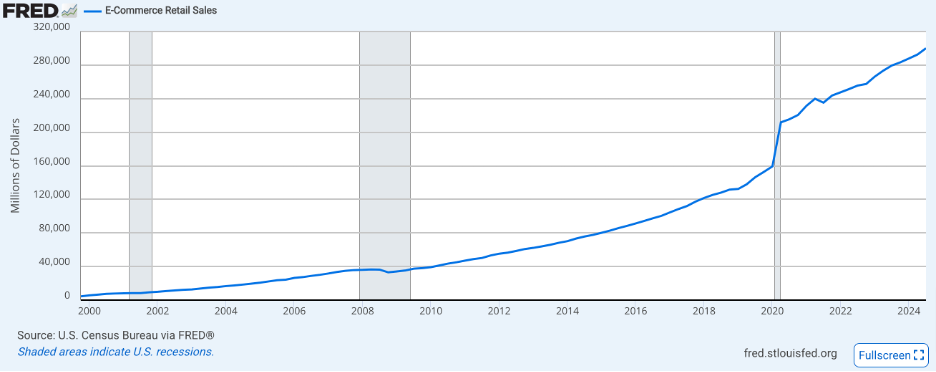

The overwhelming trend was a migration to online purchases. For example, estimates suggest that U.S. e-commerce sales grew significantly during this period—figures from various sources indicate that online sales increased by as much as 80% or more over a few short years. (Note: While one figure mentioned a growth from approximately $160 billion to $300 billion, actual numbers vary by source, but the overall trend is clear: the shift to online was dramatic.)

The overwhelming trend was a migration to online purchases. For example, estimates suggest that U.S. e-commerce sales grew significantly during this period—figures from various sources indicate that online sales increased by as much as 80% or more over a few short years. (Note: While one figure mentioned a growth from approximately $160 billion to $300 billion, actual numbers vary by source, but the overall trend is clear: the shift to online was dramatic.)

The Acceleration of Existing Trends

Many argue that COVID-19 did not so much create new consumer behaviors as it accelerated changes that were already underway. E-commerce had been steadily growing, but the pandemic condensed what might have been a decade’s worth of change into just a few months. In particular, it forced older demographics—traditionally more reliant on brick-and-mortar shopping—to embrace digital purchasing, aligning their behavior more closely with that of younger, digitally native consumers.

Generational Purchasing Patterns

Baby Boomers (Born 1946–1964):

Historically, Baby Boomers have preferred the traditional in-store shopping experience, valuing personal interaction, tactile product examination, and customer service. However, as COVID-19 led to store closures and heightened health concerns, this cohort experienced a notable uptick in online grocery orders, prescription refills, and other essential purchases (Kim & Forsythe, 2008; Verhoef, Kannan, & Inman, 2015; Pantano et al., 2020; Donthu & Gustafsson, 2020).

Generation X (Born 1965–1980):

Often seen as a transitional group, Generation X is comfortable with both online and offline shopping channels. They appreciate the convenience of digital options while still valuing in-person experiences for more complex or high-involvement purchases. In response to the pandemic, many retailers enhanced their digital services (e.g., click-and-collect and curbside pickup) alongside rigorous in-store safety protocols, thus bridging the gap between digital adoption and traditional shopping (Verhoef et al., 2015; Sheth, 2020).

Millennials (Born ~1981–1996) and Generation Z (Born ~1997 Onward):

As digital natives, Millennials and Generation Z have always been comfortable with using mobile devices, social media, and online platforms for shopping. Their behaviors—favoring speed, convenience, and seamless integration between digital and physical retail—were already well established before COVID-19. The pandemic reinforced their expectations, with these consumers demanding enhanced contactless payment options, real-time inventory checks, and smooth transitions between online and offline shopping experiences (Fromm & Garton, 2013; Kim & Forsythe, 2008; Sheth, 2020).

Conclusion

The abrupt disruption of traditional retail channels forced even reluctant consumers to overcome their technological hesitations. This “forced experiment” expanded digital literacy among older consumers and raised overall expectations for digital convenience. In response, retailers rapidly invested in digital infrastructure and omnichannel strategies—integrating enhanced safety measures in physical stores with improved online offerings—to create a more unified shopping experience.

As a retailer, meeting consumers where they are is essential. Adapting your business model to fit the new consumer expectations—particularly by strengthening your digital infrastructure—is no longer optional. The shopping landscape has irrevocably changed, and businesses must evolve to remain relevant in a world where the blend of online and offline experiences is now the norm.

References

- Donthu, N., & Gustafsson, A. (2020). Effects of COVID-19 on business and research. Journal of Business Research, 117, 284–289.

- Fromm, J., & Garton, C. (2013). Marketing to Millennials: Reach the largest and most influential generation of consumers ever. AMACOM.

- Kim, J., & Forsythe, S. (2008). Adoption of online shopping: An application of diffusion of innovation theory. Journal of Retailing and Consumer Services, 15(2), 97–110.

- Pantano, E., Pizzi, G., Scarpi, D., & Dennis, C. (2020). Competing during a pandemic? Retailers' ups and downs during the COVID-19 outbreak. Journal of Business Research, 116, 209–213.

- Sheth, J. (2020). Impact of COVID-19 on consumer behavior: Will the old habits return or die? Journal of Business Research, 117, 280–283.

- Verhoef, P. C., Kannan, P. K., & Inman, J. J. (2015). From multi‐channel retailing to omni‐channel retailing: Introduction to the special issue on multi‐channel retailing. Journal of Retailing, 93(2), 174–181.